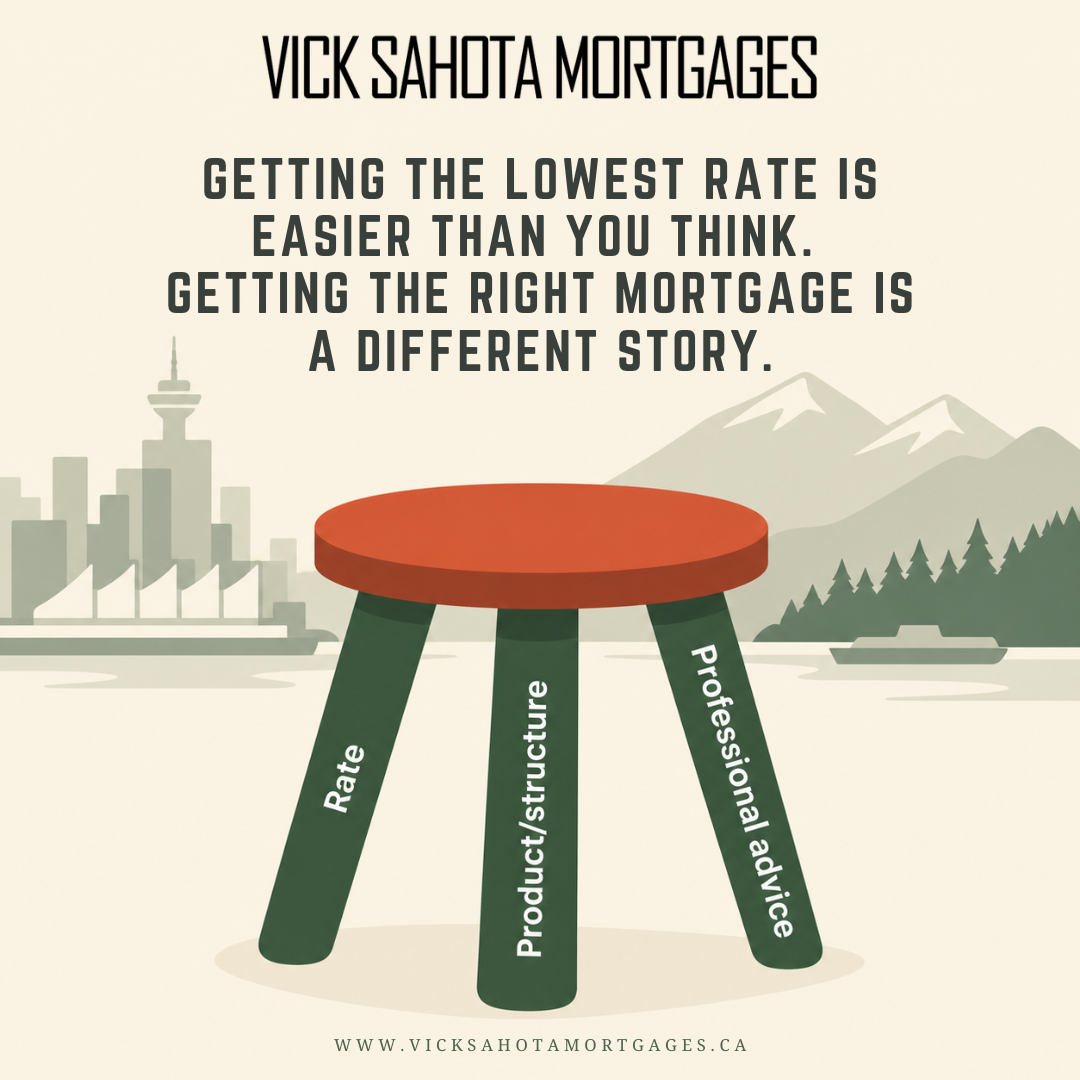

Getting the Lowest Rate in Vancouver, South Surrey & White Rock Is Easier Than You Think. Getting the Right Mortgage Is a Different Story.

If your mortgage is coming up for renewal in Vancouver, South Surrey, or White Rock, there's a good chance rate is the first thing on your mind. And that makes sense. It's the number that gets the most attention, it's the easiest to compare, and every bank is more than happy to lead with it.

But here's the problem: chasing the lowest rate is not the same as getting the best mortgage for your situation. And for local homeowners who are about to renew, that distinction matters more than most people realize.

The Rate-Shopping Playbook

You already know how this works. Go to your bank, get a quote. Take that quote to the next bank, see if they'll beat it. Repeat with every major lender. Try different branches of the same bank. Repeat a few more times. You'll definitely land a lower rate than what you started with.

And then you sign, close, and move on. Until your next renewal, when you have to do it all over again.

Here's what that process actually costs you: your time, your energy, and the assumption that a lower rate automatically means a better deal. It does not.

The Lowest Rate Is Not Always the Lowest Cost

This is the part that most borrowers don't find out until it's too late.

A rate is just one consideration in a much larger equation. The mortgage product you're in, the features you have access to, the penalty structure if your situation changes, how the mortgage aligns with where you're likely headed in the next few years. These things have real dollar implications that a slightly lower rate can't always offset.

At renewal, your bank is not always evaluating your full financial picture. They're offering you a product off a shelf. Whether it's the right product for where you are today and where you're going is a conversation that rarely occurs.

You can end the renewal process with a rate that beats every competitor and still end up in the wrong mortgage.

What Happens After You Close

Rate shopping also tends to end the moment the deal is done.

Once you sign, the bank's job is finished. There's no one monitoring whether a better opportunity opens up mid-term. No one checking on your strategy and goals. No one reaching out when market conditions shift in a way that could benefit you. You're on your own until the next renewal letter shows up in your mailbox.

For most homeowners in Vancouver and the Fraser Valley, that means leaving money on the table between renewals without knowing it.

What the Right Mortgage Actually Looks Like

The lowest cost mortgage is not just a rate. It's a combination of three things: the right rate, the right product and structure for your situation, and professional advice with active management over time.

The right rate matters, and getting a competitive rate is absolutely part of the job. But it's only one piece.

The right product and structure mean your mortgage is set up in a way that fits your life. Your income, your goals, your timeline, and what you might need flexibility for. A five-year fixed might look great on paper and be completely wrong for your situation.

And active management means someone is paying attention after the mortgage closes. Reviewing your mortgage as your life changes. Flagging opportunities. Making sure you're not sitting in a product that no longer serves you.

That's the difference between shopping for a rate and actually having a mortgage strategy.

What This Means for Your Renewal

If you have a Vancouver, South Surrey, or White Rock mortgage renewal coming up, you have more leverage than you think. But only if you use it the right way.

The renewal offer your lender sends you is not always their best offer. It's their opening move. And comparing it to what the bank down the street will offer is a start, but it's not a strategy.

The right move is to understand what you actually need from this next term, get a competitive rate that reflects current market conditions, make sure the product you're signing is built around your situation, and ensure someone actually reviews your mortgage after the fact. Not just the lowest number on a page.

Ready to Stop Managing Your Mortgage on Your Own?

If your renewal is coming up and you want to make sure you're getting the right mortgage, let's talk.

A discovery call takes about 20 minutes. We'll look at where you're at, what you need from this next term, and what your options actually look like. Book your discovery call today.