Mortgage Strategies for Vancouver, South Surrey & White Rock

Actionable mortgage advice and local market insights designed to help homeowners in British Columbia reduce interest, optimize their mortgage structure, and build long-term wealth.

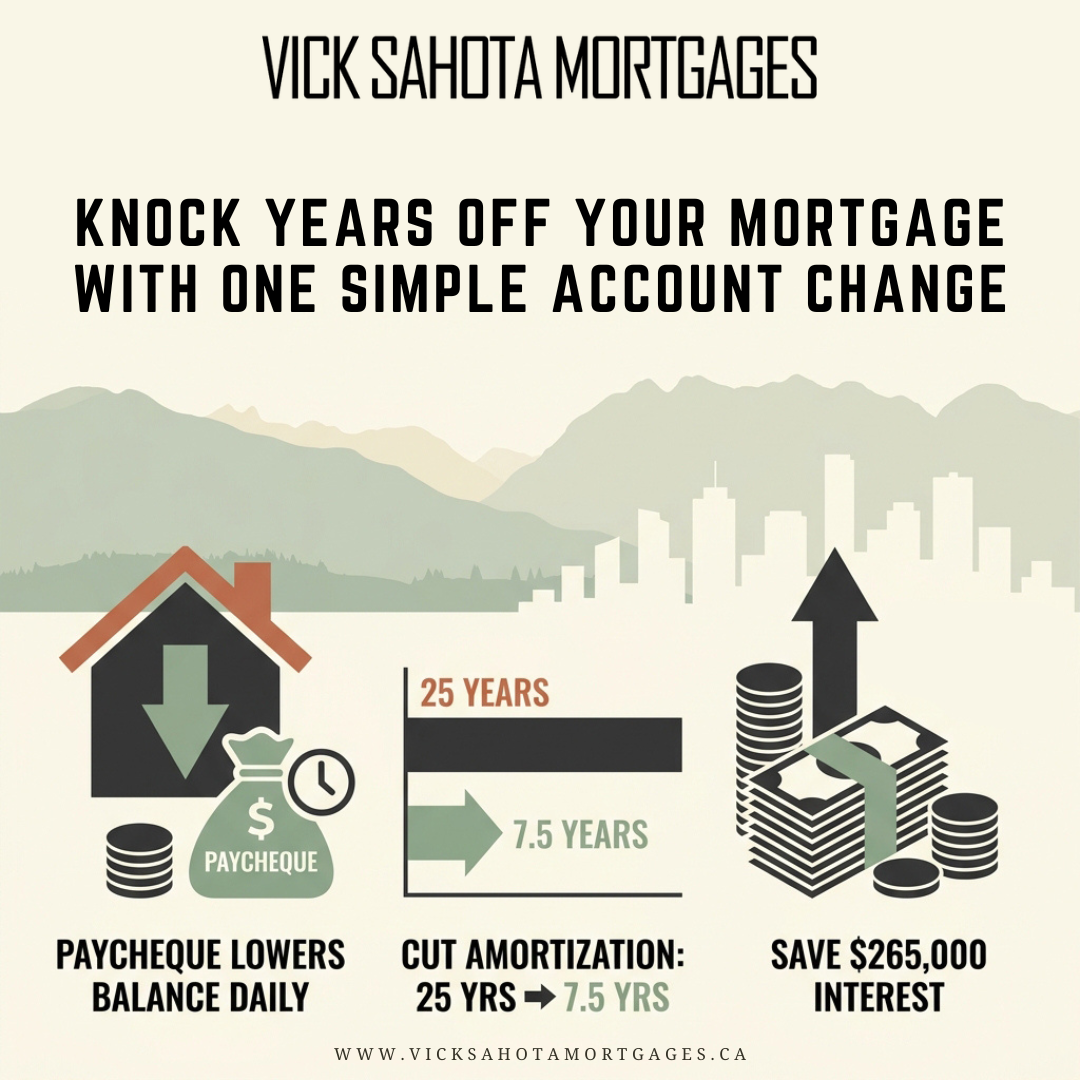

How South Surrey Homeowners Can Pay Off Their Mortgage Years Faster With an Offset Mortgage Strategy

South Surrey homes tend to come with higher prices, and with that comes larger mortgage balances. Yet, most local homeowners have money sitting in a chequing account doing nothing while their mortgage charges interest on that substantial balance every single day. Your income and your mortgage never work together, and on a larger mortgage, that gap quietly costs you thousands.

The offset mortgage strategy closes that gap. Here is how it works and whether it could be a fit for your situation.

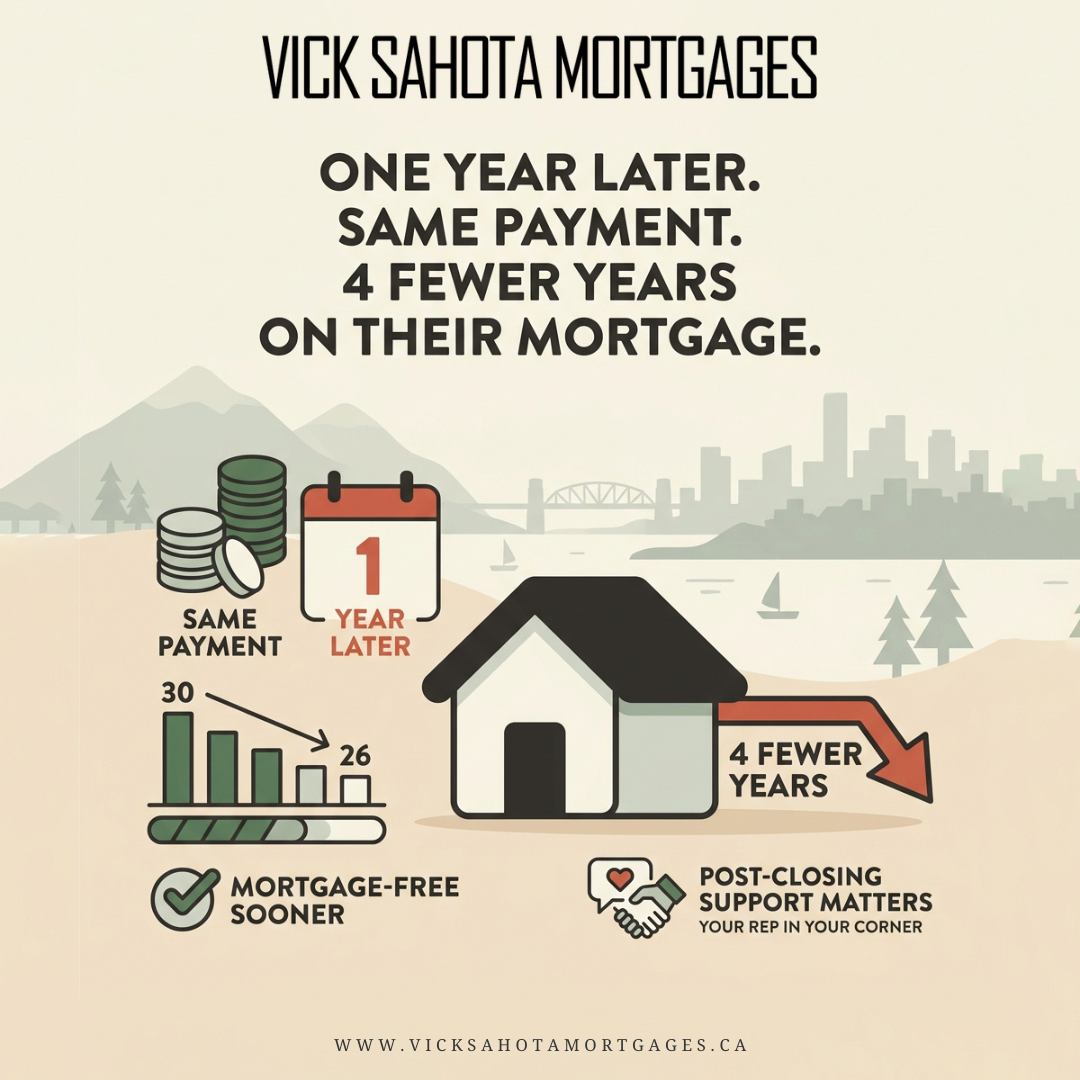

Your Vancouver Mortgage Funded. Now What? Why Post-Closing Support Changes Everything.

Most People Assume Their Mortgage Is a Set-It-and-Forget-It Decision

You sign the papers, the mortgage funds, and then you move on with your life. The bank processes your payments automatically. Everything seems fine. But fine is not the same as optimal, and the gap between the two can quietly cost you thousands over the life of your mortgage.

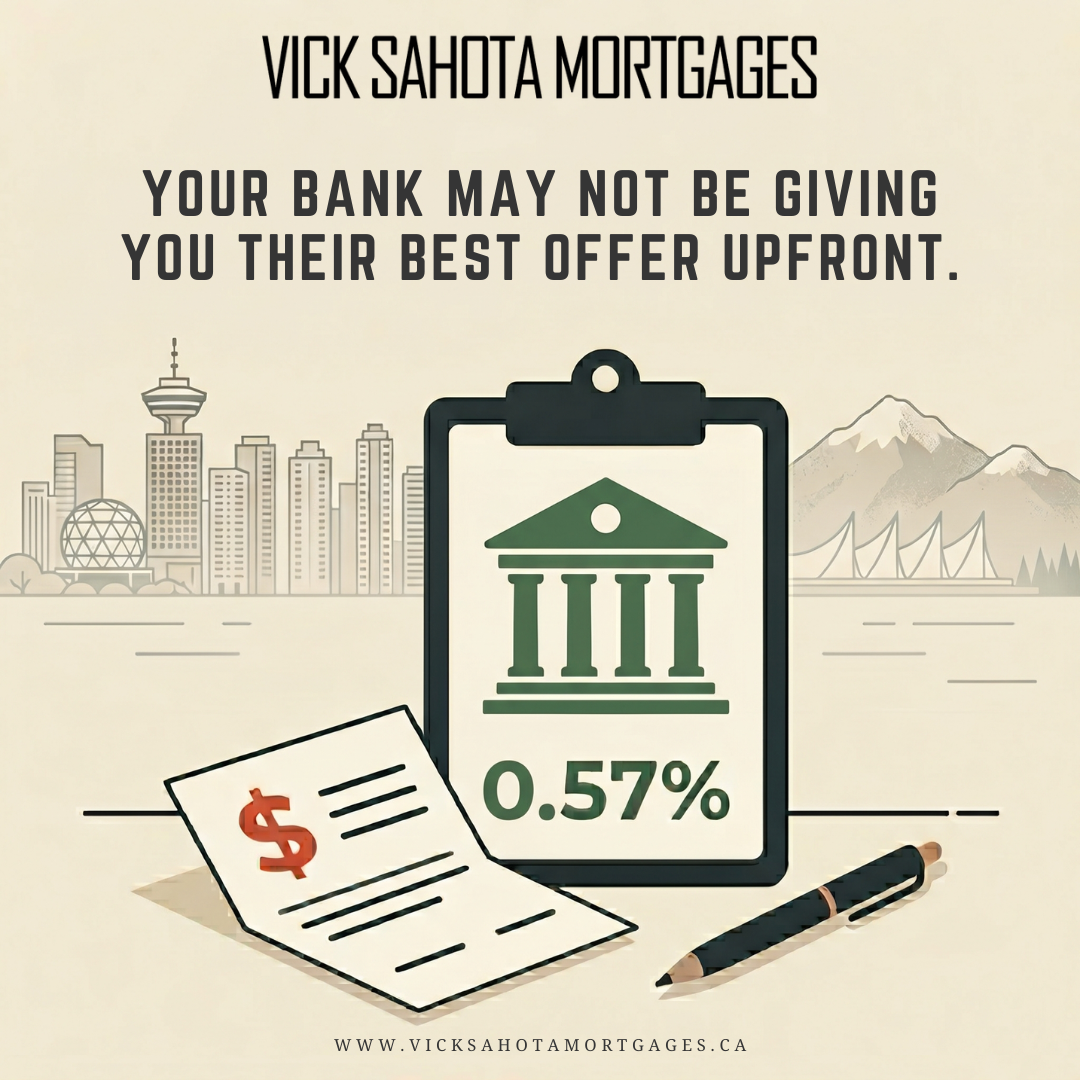

Is Your Bank Really Giving You Their Best Mortgage Offer?

What Vancouver, South Surrey, and White Rock homeowners need to know before signing their renewal or refinance.

If your mortgage is coming up for renewal, your bank will reach out with an offer. It will look professional, the numbers will seem reasonable, and there will likely be a deadline attached to create a sense of urgency. But here is the question worth asking before you sign anything: Is that actually their best offer?

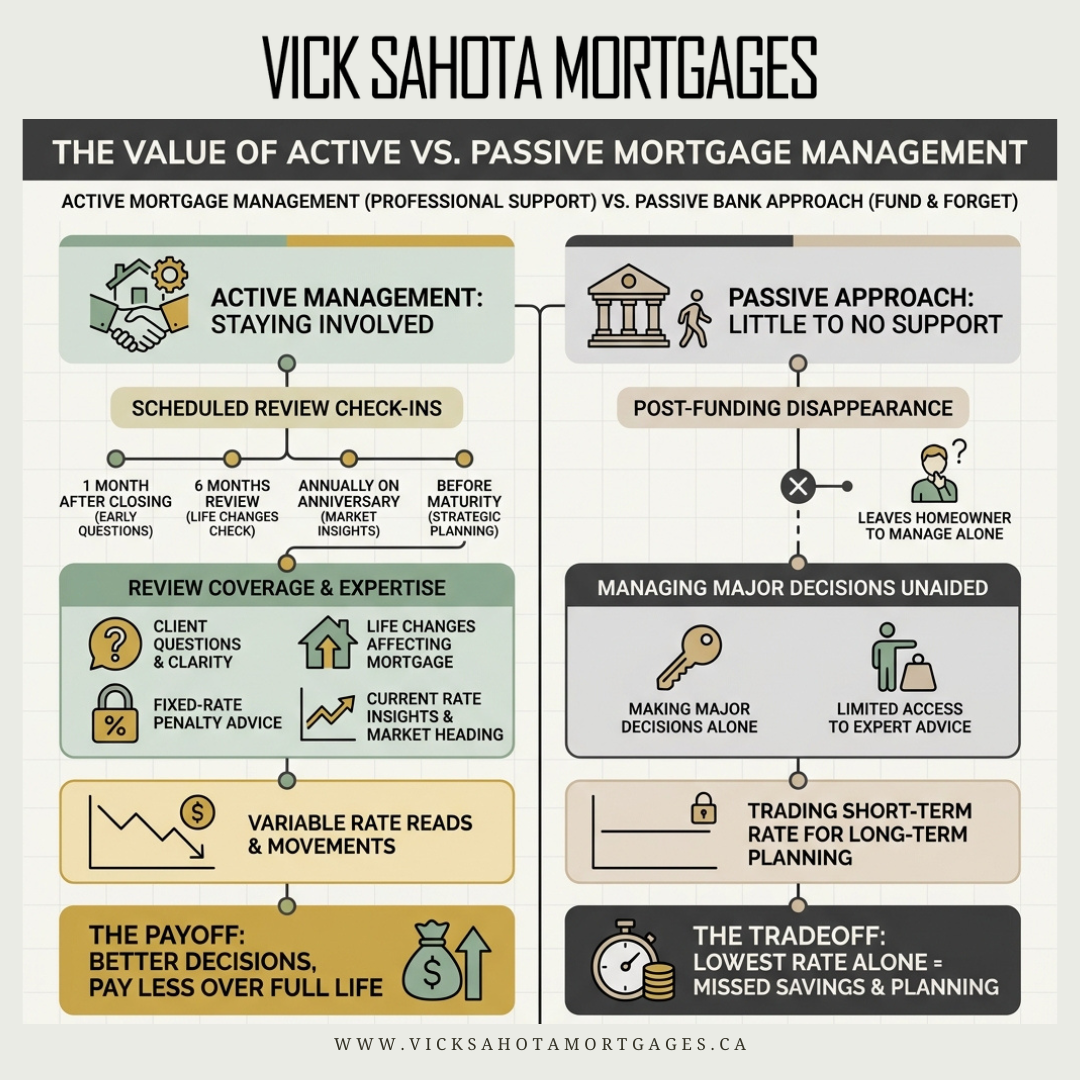

Who Is Actively Managing Your Mortgage in Vancouver, South Surrey & White Rock?

Most homeowners only think about their mortgage at two points: when they first get it, and when it comes up for renewal. The years in between are usually treated as a stretch where nothing needs attention. Unfortunately, that gap is where a lot of money is quietly lost, and it is the part of the mortgage process that gets the least support.

For homeowners in Vancouver, South Surrey, and White Rock, where property values and mortgage balances are among the highest in the country, the cost of being left on your own through the middle of a term is real. The difference between a mortgage that is actively managed and one that is left to sit can easily add up to thousands of dollars over time.

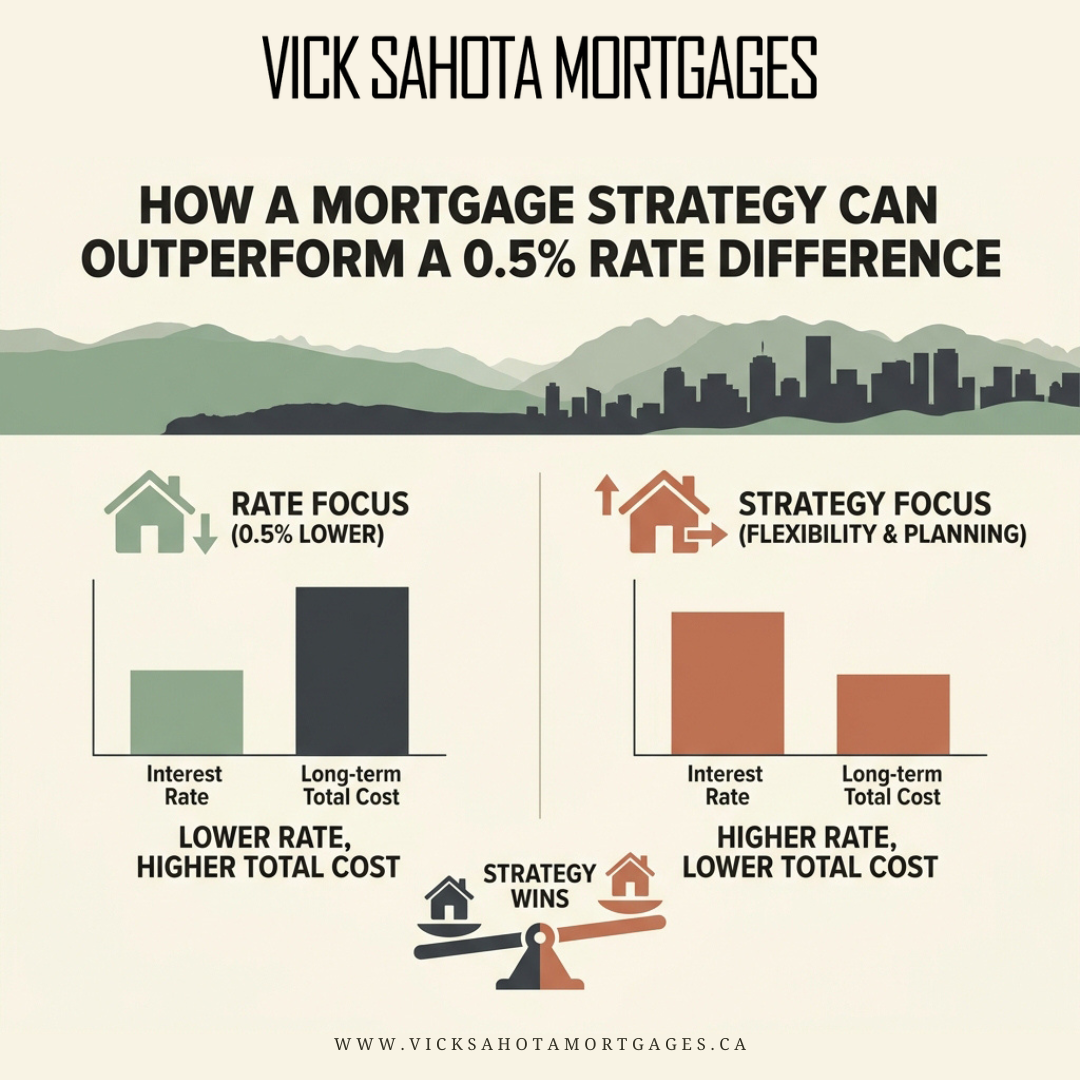

How a Mortgage Strategy Can Outperform a Lower Rate: A Guide for Vancouver, South Surrey and White Rock Homeowners

Most homeowners across Vancouver, South Surrey and White Rock approach the mortgage process with one question at the top of mind: what is the lowest rate available? Rate shopping has become the default behaviour at both the purchase stage and the Vancouver mortgage renewal stage, often pursued at the expense of every other variable that affects long-term financial outcomes.

The reality is that the strategy attached to a mortgage drives long-term wealth outcomes far more meaningfully than the headline interest rate. A side-by-side comparison of two homeowners with identical $500,000 mortgages on 30-year amortizations illustrates the point clearly.

What If Your Tax Refund Could Generate More Tax Refunds Every Single Year?

With the tax deadline behind us, many homeowners across British Columbia, from Vancouver to South Surrey and White Rock, have refunds coming their way.

For most people, that money gets absorbed into everyday spending without much thought. But if you own real estate, your tax refund can be more than just a one-time cash injection. It can be a powerful wealth-building tool that you put to work year after year.

Here are a few smart ways to maximize your tax refund as a BC homeowner.

The Real Cost of Your Mortgage: What Vancouver, South Surrey & White Rock Homeowners Need to Know

Rate is the number that gets advertised, compared, and negotiated with mortgages. But after working with homeowners across Vancouver, South Surrey, and White Rock, I can tell you that rate is only part of the story. The real cost of your mortgage plays out over the life of the loan, and a lot of that depends on what happens after you close.

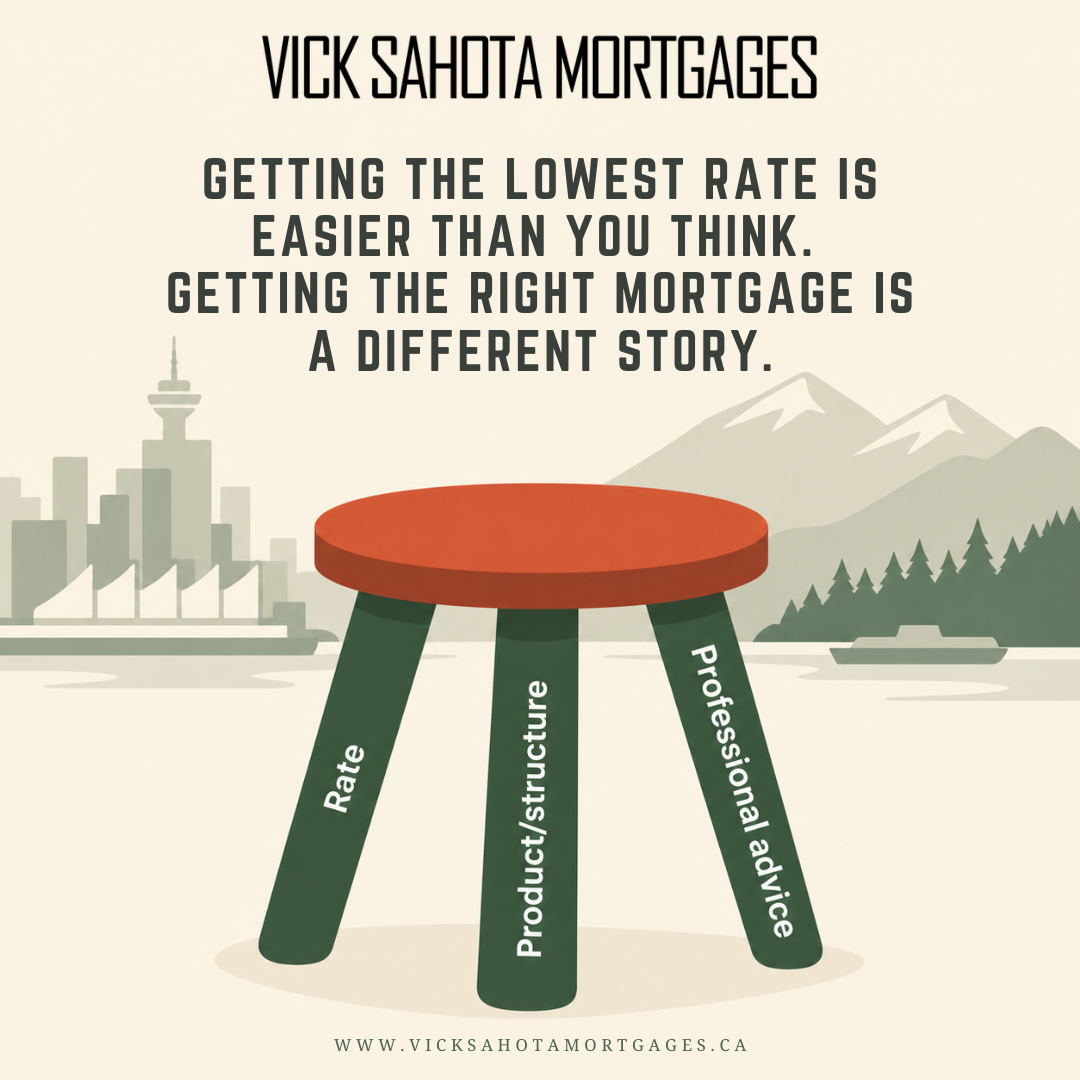

Getting the Lowest Rate in Vancouver, South Surrey & White Rock Is Easier Than You Think. Getting the Right Mortgage Is a Different Story.

If your mortgage is coming up for renewal in Vancouver, South Surrey, or White Rock, there's a good chance rate is the first thing on your mind. And that makes sense. It's the number that gets the most attention, it's the easiest to compare, and every bank is more than happy to lead with it.

But here's the problem: chasing the lowest rate is not the same as getting the best mortgage for your situation. And for local homeowners who are about to renew, that distinction matters more than most people realize.

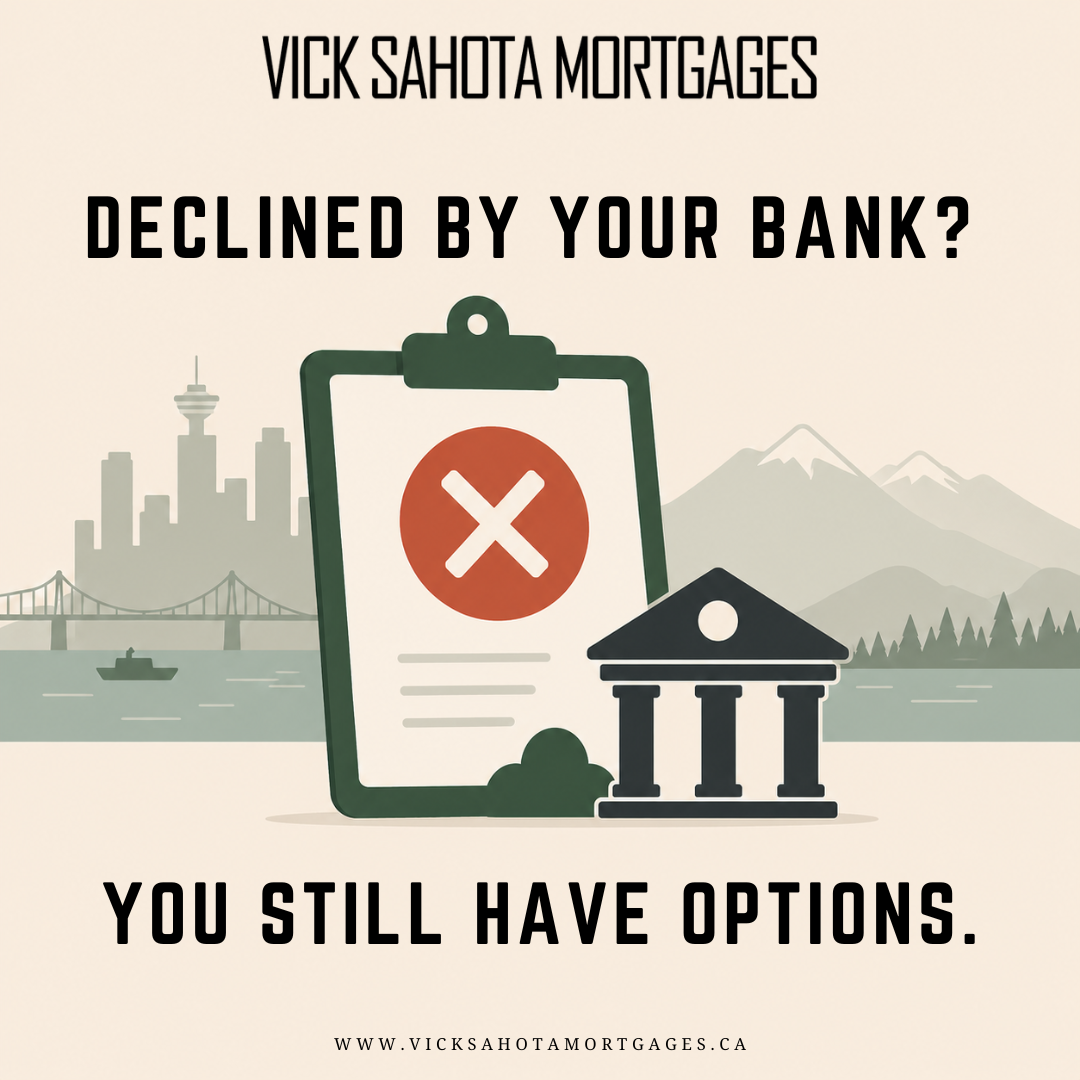

Declined By Your Bank? You Still Have Options

A decline from your bank feels final. It is not. Every lender in Canada operates with its own risk appetite and underwriting guidelines. The file your bank passes on can be the same file another lender approves. Here is how repositioning works, with real client scenarios from the Vancouver market.

The Right Mortgage Strategy Does Not End on Closing Day

Most people think the mortgage process ends when the deal closes. It does not. At least, it should not.

One of the biggest gaps in the mortgage industry is what happens after closing day. For clients who work with the big banks, the answer is usually nothing. No check-in. No review. No call to let you know that rates have shifted, that your penalty is about to drop, or that there is a strategy available to save you thousands of dollars in interest. You are on your own.

That is not how I work.

Mortgage Paydown vs. Investing in Vancouver: What the Math Actually Says (And Why Most Homeowners Get It Wrong)

If you own a home in the Lower Mainland, you already know that a massive portion of your monthly cash flow goes toward housing. For decades, the traditional Canadian approach has been simple: pay off your mortgage as fast as humanly possible.

But is that actually the best way to build wealth?

When you sit down and run the numbers, the "debt-free at all costs" mentality can actually result in you leaving hundreds of thousands of dollars on the table, or worse, retiring "house rich but cash poor." Let’s look at a different strategy for your mortgage paydown and see what the math actually says.

Why You Need a Strategic Vancouver Mortgage Advisor for Your Home Purchase

Buying a home in Vancouver is an incredible milestone, but let’s be honest: it’s also an incredibly expensive one. With our city's premium real estate prices comes the reality of large mortgage sizes. If you are stepping into this market, especially as a first-time home buyer with no prior purchasing experience, the sheer size of the debt can feel overwhelming.

It is completely natural to want the easiest path forward, which for many means walking into their long-time bank and asking for a loan. However, simply getting a mortgage and actively managing it to build wealth are two completely different things.

Here is why you should think twice about fixating solely on interest rates, and why partnering with a strategic mortgage advisor is one of the smartest financial moves you can make.

The Hidden Costs of a 5-Year Fixed Mortgage in Vancouver: Why the "Safe" Choice Could Cost You Thousands

Five years is a long time to lock in, especially if no one is actively managing your mortgage. Many homeowners opt for the “safe” 5-year fixed-rate mortgage with their bank, thinking it’s their best option.

However, in many cases, there is zero discussion from the bank about your actual goals and what your plans are for the next five years. A lot can change in that time, including moving to a new home, and market rates may be completely different down the road.

If at any point you need to break your mortgage, you may be hit with a massive penalty on that 5-year fixed contract. Your bank won’t let you know when it’s best to break your mortgage to pay less of a penalty, or if there’s ever a savings opportunity. When you go directly to the bank for your mortgage, it’s entirely up to you to self-manage it as proactive management is usually non-existent.

Vancouver Mortgage Renewal Playbook for 2026

If your mortgage term is coming to an end in 2026, you are part of a massive wave of Canadian homeowners facing a vastly different interest rate landscape than when you first signed your contract in 2021.

Approaching a mortgage renewal in Vancouver can feel daunting, especially with the rising cost of living and shifting property values. But a renewal isn't just a piece of paper to sign, it is one of the most critical financial windows of opportunity you have.

Whether you are worried about cash flow, considering pulling out equity, or just want to ensure you aren't being taken advantage of by your current bank, this playbook will walk you through exactly how to navigate your 2026 renewal.

Stop Giving the Bank Free Money: How an Offset Mortgage Works

Most people have their paycheque deposited into a regular chequing account where it does nothing for them. At the same time, they’re carrying a mortgage balance that is costing them interest every single day. An offset mortgage can be a smart way to reduce that interest and pay down your mortgage faster without changing your lifestyle.

At its core, an offset mortgage combines your chequing account, line of credit, and mortgage into one product. That means your money can start working for you the moment it hits the account.

Don’t Sign That Vancouver Mortgage Renewal Letter Just Yet…

Mortgage renewals can feel deceptively simple: your lender sends you an offer, you sign it, and life goes on. But under the surface, a rushed or uninformed renewal can cost you thousands in interest and future penalties, lock you into the wrong product, and completely ignore your evolving financial goals.

The truth is, a mortgage renewal is not just a transaction. It’s a great opportunity to realign your finances and make better moves. I’ll go over what you need to know about your Vancouver Mortgage renewal, and why having a professional mortgage advisor in your corner could be the smartest financial decision you make this year.

Mortgage Renewals in BC: Guidance Before You Sign Anything

If you’re looking to renew your mortgage, here’s 3 important considerations that you should think about before signing that renewal letter. A renewal is a decision point, and it’s worth looking at it strategically, not just as a quick “sign and send back” moment.

How One Client Will Pay Off Their Mortgage 10 Years Faster

When most people think of getting a mortgage, they think of one thing: getting the lowest rate. But if that was all that mattered, this client wouldn't be on track to pay off their mortgage years sooner than originally planned.

I have a client who got a 25-year mortgage back in 2023. Fast forward just 2.5 years later, and their mortgage is already set to be paid off in 18 years. Eventually, I believe we’ll bring that timeline down even further to 12–15 years. Here's how we did it:

HOW STATIC-PAYMENT VARIABLE MORTGAGES CAN SLASH YOUR AMORTIZATION IN A RATE-DROP CYCLE

Here’s a real-world case study that highlights the upside of a static-payment variable mortgage in a rate-decreasing environment.

Why the Lowest Mortgage Rate Can End Up Costing You More

Homeowners often fixate on getting the lowest mortgage rate, but rate alone doesn’t determine the true cost of your mortgage. The penalty structure, product flexibility, and lender policy can have a much bigger financial impact than most people realize.