How a Mortgage Strategy Can Outperform a Lower Rate: A Guide for Vancouver, South Surrey and White Rock Homeowners

Most homeowners across Vancouver, South Surrey and White Rock approach the mortgage process with one question at the top of mind: what is the lowest rate available? Rate shopping has become the default behaviour at both the purchase stage and the Vancouver mortgage renewal stage, often pursued at the expense of every other variable that affects long-term financial outcomes.

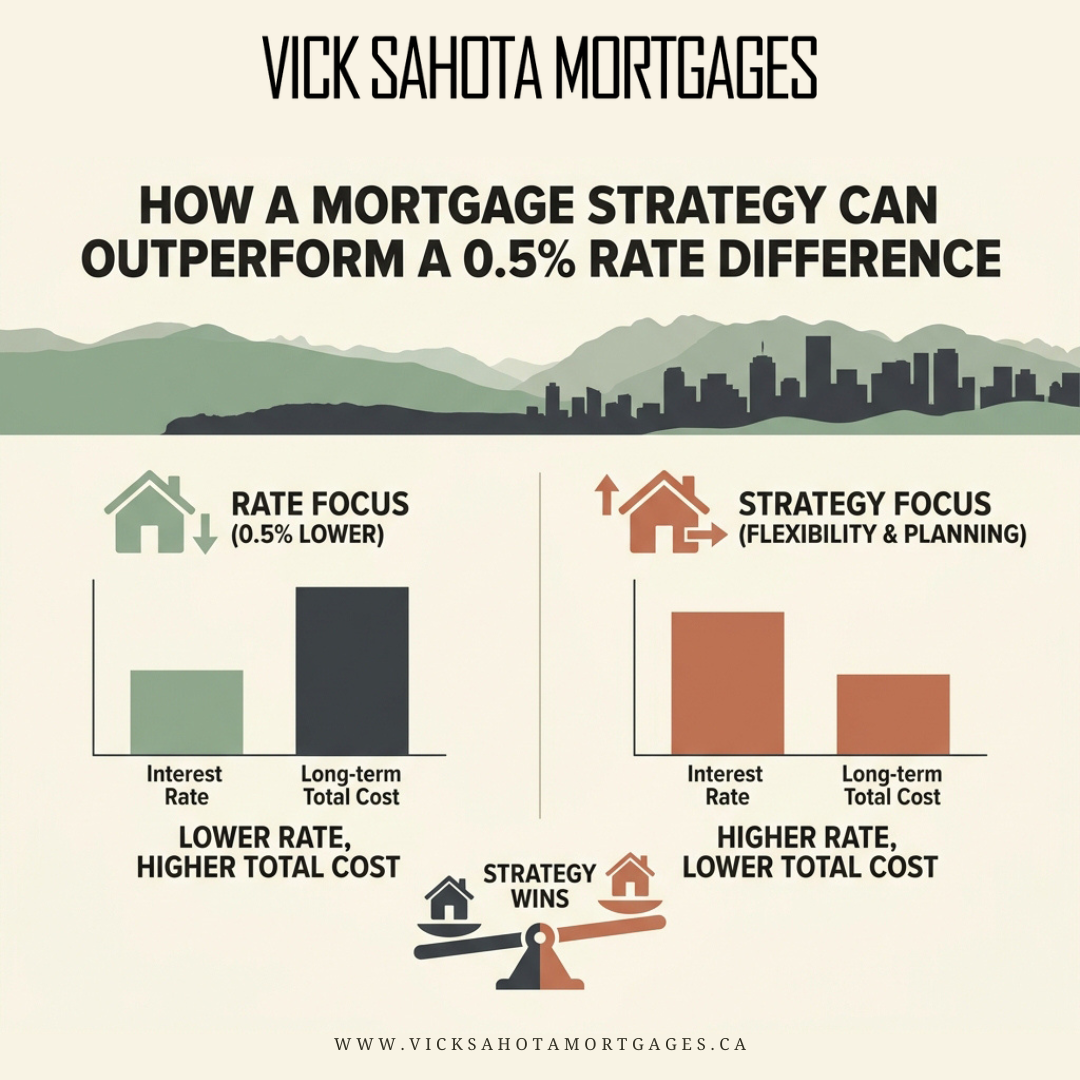

The reality is that the strategy attached to a mortgage drives long-term wealth outcomes far more meaningfully than the headline interest rate. A side-by-side comparison of two homeowners with identical $500,000 mortgages on 30-year amortizations illustrates the point clearly.

Why the Lowest Mortgage Rate Doesn't Always Produce the Best Outcome

A mortgage is one of the largest financial commitments most households take on, particularly in markets like Vancouver, South Surrey and White Rock where average property values support six-figure mortgage balances and meaningful long-term interest exposure. Focusing on rate alone is a narrow lens for evaluating a financial commitment of that size.

The interest rate determines the monthly payment and the total interest paid over the life of the mortgage. The strategy determines whether that mortgage can be used as a vehicle to build wealth at the same time. Two mortgages can produce dramatically different financial outcomes depending on the structure and a wealth-building mortgage strategy applied to them.

Scenario One: A Conventional 4% Mortgage With No Strategy

The first homeowner secures a 4% mortgage at $2,377.59 per month and follows the standard amortization path. There is no refinancing along the way and no investment activity tied to the mortgage. The mortgage renews every five years at the same rate until the loan is fully paid off in 30 years.

Over the 30-year period, this homeowner pays approximately $356,000 in non-deductible interest. There is no investment portfolio, no recovered tax refunds, and no additional financial asset built alongside the property.

At the 26-year mark, the homeowner still owes approximately $105,000 in mortgage principal and has $0 in investments. The home is on track to be paid off in four more years, but no other retirement portfolio has been built during the process.

Scenario Two: A Higher 4.5% Mortgage With a Wealth-Building Strategy

The second homeowner accepts a higher 4.5% mortgage at $2,521 per month. The strategy applied to this mortgage works as follows: Each month, as the mortgage principal is paid down, an equivalent amount is re-borrowed through a Home Equity Line of Credit and invested into a portfolio of assets with a reasonable expectation of generating income.

Because the borrowed funds are used for investment purposes with the reasonable expectation of generating income, the interest on the line of credit becomes tax-deductible under Canada Revenue Agency rules. The tax refund generated each year by deducting that interest is then applied as a prepayment against the mortgage, which materially accelerates the paydown.

After 26 years, the mortgage is fully converted into a tax-deductible loan of $500,000. The investment portfolio sits at approximately $604,000. Approximately $84,000 in cumulative tax refunds have been recovered along the way, which are used to prepay the mortgage.

Netting the $500,000 tax-deductible loan against the $604,000 investment portfolio, the homeowner is in a net positive financial position of approximately $100,000 (not factoring in any tax implications). That is in addition to the home itself. The homeowner who paid the higher rate ends up materially wealthier because of the strategy attached to the mortgage.

What About Simply Investing the Rate Savings?

A common counterargument is that the homeowner with the lower 4% rate could simply take the $143 monthly payment difference and invest it on the side at the same 6.4% rate of return assumed for the strategy above. Over 26 years, this approach produces an investment portfolio of approximately $115,000. After accounting for the $105,000 of mortgage principal still outstanding at the 26-year mark, the homeowner is in a net positive financial position of only approximately $9,000.

That outcome is still better than no investment activity at all, but it falls dramatically short of the strategy-based approach. The reason is structural. The wealth-building strategy puts $500,000 of borrowed capital to work in the market and recovers tax refunds along the way. Simply investing the rate savings on the side only puts $143 per month to work and generates no tax recovery. The same monthly cash outlay over 26 years produces two very different wealth outcomes.

Why This Matters Specifically for Vancouver, South Surrey and White Rock Homeowners

The takeaway for homeowners in these markets is straightforward. Mortgages in these markets tend to be higher, and substantial interest is paid over the life of the mortgage. Sometimes, nothing is left over for retirement savings and after years of paying off the mortgage, homeowners can end up with no retirement savings. By implementing a strategy like the one mentioned in this blog post, homeowners in these markets can pay off their homes quicker, convert their mortgages into tax-deductible loans, build a portfolio of assets for retirement, all with no additional cash out of pocket.

A mortgage at renewal or at purchase is more than just a rate. Implementing a tailored mortgage strategy in Vancouver can determine whether your household financial plan consumes wealth through 30 years of non-deductible interest or builds substantial wealth alongside the property.

Important Considerations Before Implementing the Strategy

The numbers in this article are based on projected assumptions including a 6.4% investment return, a 35% marginal tax rate, and a 4.95% line of credit rate. Actual outcomes will vary based on market performance, individual tax circumstances, rate environment, and consistency of execution.

Several factors should be considered carefully:

Investment markets do not produce 6.4% returns every year and real-world returns are volatile and can include negative years that impact the strategy's economics.

The strategy requires discipline through monthly re-borrowing, annual tax filing of the interest deduction, and proper separation of investment funds from personal funds.

Suitability depends on individual circumstances including income stability, risk tolerance, marginal tax rate, and time horizon.

Tax laws and rate environments can change and the deductibility framework, while stable for decades, is subject to policy revision.

A suitability review with a licensed mortgage broker and a qualified financial professional is recommended before implementing the strategy. Tax implementation should be reviewed by an accountant to ensure the strategy is executed correctly.

The Bottom Line for Homeowners

For homeowners across the Lower Mainland weighing renewal options or financing a new purchase, the lesson is clear: Rate matters, but strategy matters more. A 0.5% difference in your mortgage rate is a small variable compared to whether a wealth-building strategy is attached to the mortgage in the first place.

The homeowner who pays a slightly higher rate but applies the right strategy can end up materially wealthier than the homeowner who simply chases the lowest available rate. That difference compounds over time and shows up in the form of a six-figure investment portfolio, a tax-deductible loan structure, and tens of thousands of dollars in recovered tax refunds.

If you are a homeowner in Vancouver, South Surrey, or White Rock who is serious about your financial goals, a licensed mortgage broker who understands both the loan product and the wealth-building mechanics is the right starting point. Click the button below to book a call.