Your Vancouver Mortgage Funded. Now What? Why Post-Closing Support Changes Everything.

Most People Assume Their Mortgage Is a Set-It-and-Forget-It Decision

You sign the papers, the mortgage funds, and then you move on with your life. The bank processes your payments automatically. Everything seems fine. But fine is not the same as optimal, and the gap between the two can quietly cost you thousands over the life of your mortgage.

Here is the reality: once your mortgage funds, your bank is not checking in on you. No one is reviewing whether your current product still fits your situation. No one is flagging opportunities to save or warning you about decisions that could work against you. You are on your own, and most homeowners in Vancouver, South Surrey, and White Rock do not realize this until it is already costing them.

This is the gap that post-closing mortgage support is designed to close.

What a One-Year Mortgage Review Actually Looks Like

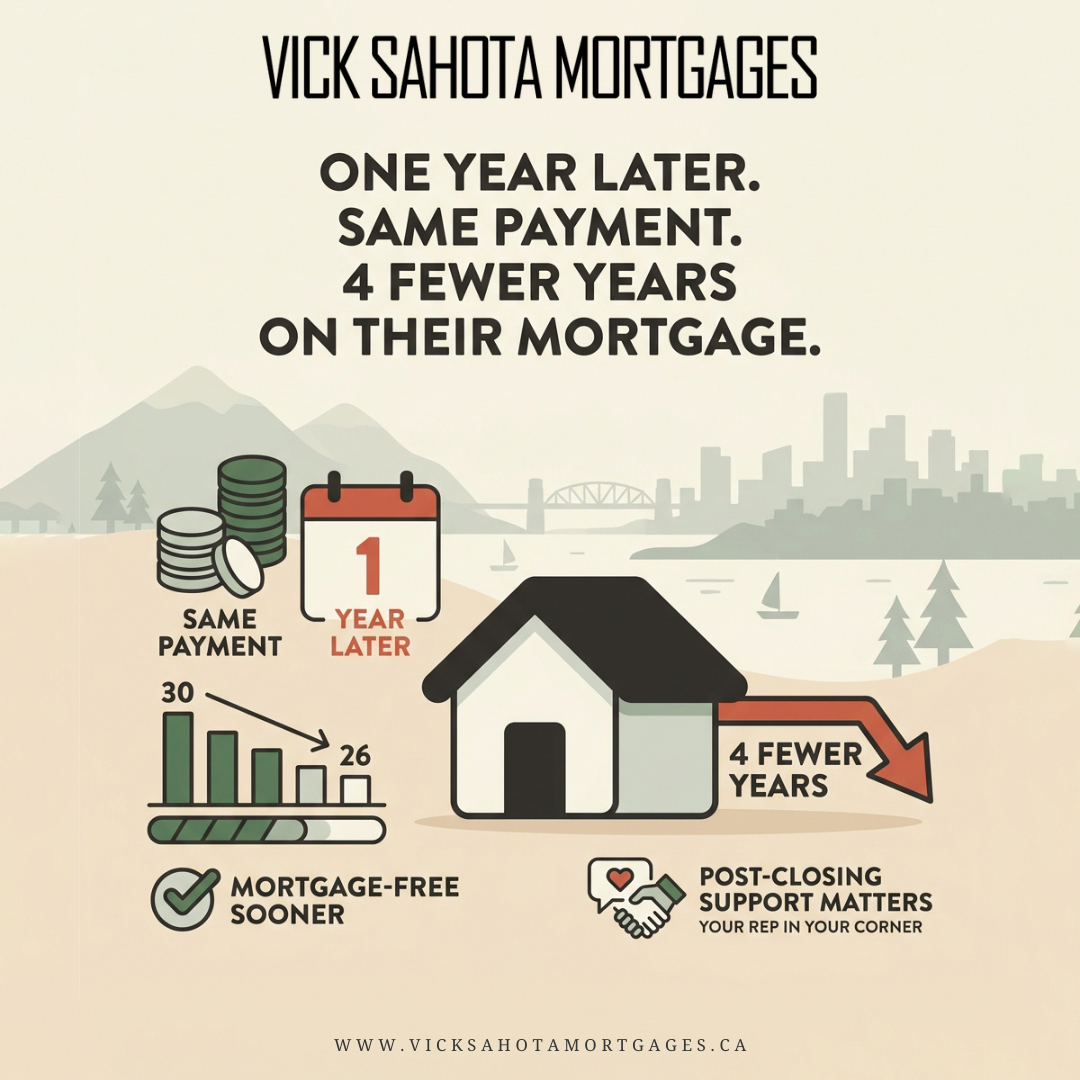

I recently completed a one-year review with a client who had chosen a static payment variable rate mortgage when we first worked together. Twelve months later, here is where things stood.

The prime rate dropped after their mortgage funded. Because they were on a static payment variable, their monthly payment stayed exactly the same. What changed was the allocation. More of each payment was now going toward the principal rather than interest. That is one of the key advantages of a static payment variable product when rates move in your favour.

When we first set up their mortgage, they were on a 30-year amortization. One year in, they are now on track to pay off their mortgage in approximately 26 years. That is four years shaved off without changing their payment or doing anything differently. That outcome happened because the right product was chosen at the start.

One thing worth understanding about static payment variables: if the prime rate increases, the opposite dynamic occurs. Your payment stays the same, but more of it goes toward interest and less toward principal, which means your amortization can extend. It is not a reason to avoid the product. It is a reason to understand it and have someone monitoring it.

The Conversation That Followed

During the review, I walked my client through exactly where their mortgage stood. Their current rate is still very competitive. There are no savings opportunities that would make sense to act on right now. Their mortgage is still the right fit.

That conversation took less than 5 minutes. But what it gave them was clarity. They know where they stand. They are not guessing, not reading headlines and wondering if they should be doing something different, and not making decisions without proper context.

We scheduled the next check-in for the following year. Between now and then, they have full access to me if anything changes. A job change, a refinance question, a rental property, a life event that affects their financial picture. None of those things require waiting for an annual call.

Why This Matters to You

If you currently have a mortgage, ask yourself a simple question. Has anyone reviewed it with you in the past year? Not a renewal notice. Not an automated email. An actual conversation where someone looked at your product, your rate, your amortization, and your current situation, and told you clearly whether you are on track or whether something should change.

For most homeowners in South Surrey, White Rock, and across Vancouver, the answer is no. And that silence has a cost. Savings opportunities go unnoticed. Life changes that should trigger a mortgage review do not. Decisions get made without guidance because there is no one providing it.

The bank is not going to call you. That is not how the model works. The support you receive after closing is usually non-existent. What happens after that is entirely up to you, unless you have a broker who makes it their responsibility.

Post-Closing Support Is Not a Bonus. It Is Part of the Strategy.

Choosing the right mortgage product at the start matters. Monitoring it over time matters just as much.

Markets shift. Rates move. Life changes. A mortgage that was the right fit on day one may need to be revisited at year two or three. Or it may still be exactly right, and the value is simply knowing that with confidence rather than hoping for the best.

Working with an independent mortgage broker means you have someone whose job extends past funding day. Reviews, check-ins, market context, and access whenever something comes up. That is not a service upgrade. That is what proper mortgage advice and support looks like.

If you are looking to get a mortgage and want that level of support built in from the start, book a call below.