How South Surrey Homeowners Can Pay Off Their Mortgage Years Faster With an Offset Mortgage Strategy

South Surrey homes tend to come with higher prices, and with that comes larger mortgage balances. Yet, most local homeowners have money sitting in a chequing account doing nothing while their mortgage charges interest on that substantial balance every single day. Your income and your mortgage never work together, and on a larger mortgage, that gap quietly costs you thousands.

The offset mortgage strategy closes that gap. Here is how it works and whether it could be a fit for your situation.

The Problem With a Traditional Mortgage

Your paycheque lands in your chequing account and earns next to nothing. At the same time, your mortgage charges interest on the entire outstanding balance, day after day. Your cash and your mortgage operate as two separate systems that never communicate.

Prepayments help, but once you make them, that money is locked into your home. You lose access to it. For most South Surrey homeowners, that tradeoff between paying down the mortgage and keeping cash accessible is the reason they leave the surplus sitting idle.

How the Offset Mortgage Strategy Works

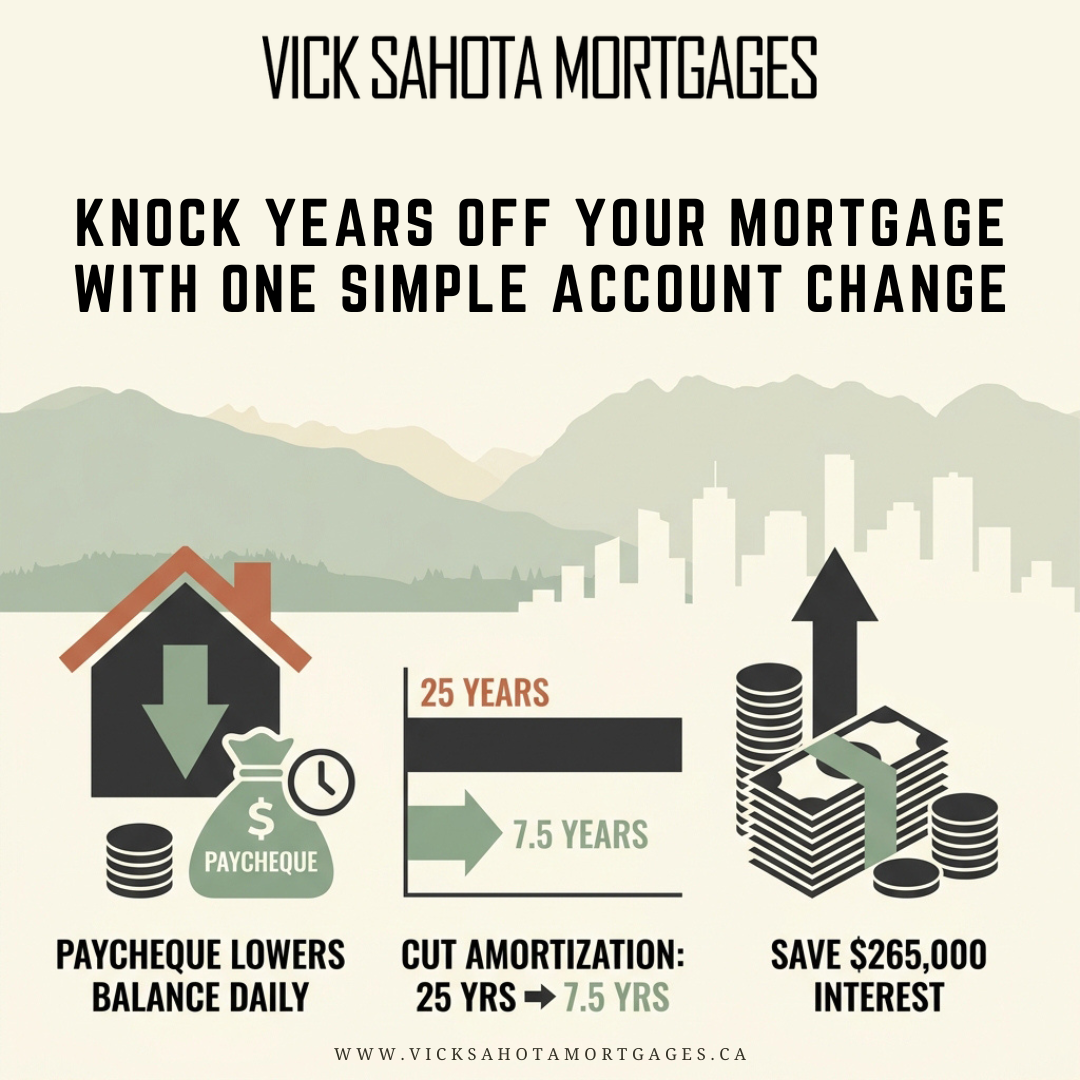

An offset mortgage combines your primary bank account with your mortgage into one structure. Your paycheque deposits directly into it. The moment that money lands, it offsets your mortgage principal and reduces the interest you are charged that day.

Here is what makes it different:

Your money works against your mortgage automatically. Every dollar you deposit lowers the balance your interest is calculated on, every single day.

It functions like a normal chequing account. Debit, e-transfers, bill payments, and full access to your cash whenever you need it.

You keep your liquidity. Your funds stay fully accessible, so you are never choosing between paying down your home and keeping an emergency fund.

Until the moment you spend it, every dollar in the account is working to reduce your interest costs.

What This Looks Like in Real Numbers

I recently ran the numbers for a homeowner whose top priority was paying off their mortgage sooner. By using their paycheque and monthly surplus, they could shift from a 25-year amortization down to 7.5 years. Their required monthly payment would be lower, and they would save approximately $265,000 in interest over the life of the mortgage.

That example is aggressive. Even a less aggressive approach can drop the amortization significantly and save a substantial amount in total interest paid to the bank.

Who the Offset Mortgage Strategy Is For

This strategy is not for everyone. In the wrong hands, it can do more damage than a traditional mortgage. It works for a specific type of homeowner.

Your goal is to pay off your mortgage as quickly as possible and pay less total interest.

You consistently earn more than you spend each month.

You are disciplined with money and do not spend simply because credit is available.

You have strong credit and stable, provable income.

If easy access to a large credit limit feels like an invitation to spend, this structure will work against you. The discipline is what makes the math compound in your favour.

See What This Could Do for Your South Surrey Mortgage

If this is something that could work for your situation, fill in this form and I'll send over a report for your situation going over the numbers, including how many years and how much interest an offset strategy could realistically take off your mortgage.