Vancouver Mortgage Renewal Playbook for 2026

If your mortgage term is coming to an end in 2026, you are part of a massive wave of Canadian homeowners facing a vastly different interest rate landscape than when you first signed your contract in 2021.

Approaching a mortgage renewal in Vancouver can feel daunting, especially with the rising cost of living and shifting property values. But a renewal isn't just a piece of paper to sign, it is one of the most critical financial windows of opportunity you have.

Whether you are worried about cash flow, considering pulling out equity, or just want to ensure you aren't being taken advantage of by your current bank, this playbook will walk you through exactly how to navigate your 2026 renewal.

What Actually Happens at Renewal (And What Doesn't)

As your term nears its end, you will likely receive a renewal offer in the mail from your current lender. Sometimes, they don't send one at all until the very last minute.

Here is the reality of that letter:

It is rarely their most competitive rate. Lenders sometimes bank on the fact that most homeowners will simply sign the paper to avoid the hassle of shopping around. I’ve seen this first-hand, where a homeowner was offered an above-market 5-year fixed, and they unknowingly signed.

It lacks personalized advice. There is rarely a conversation about your changing life goals, cash flow needs, or long-term wealth strategy.

It isn't a strategy. A rate alone is not a strategy.

If you just sign on the dotted line, you are likely leaving money and flexibility on the table.

The Renewal Timeline: Why Being Early Matters

You shouldn't wait for your lender's letter to start planning. Time is your greatest asset when it comes to securing the best terms.

120 Days Out: This is the critical window. Most lenders can hold a rate for up to 120 days (roughly 4 months). This protects you from rate hikes while you finalize your decision. If rates drop before your closing date, a good broker will ensure you get the lower rate.

Early Renewal: In some scenarios, especially if rates are forecasted to increase, it may make mathematical sense to break your mortgage early, pay the penalty, and lock in a new rate.

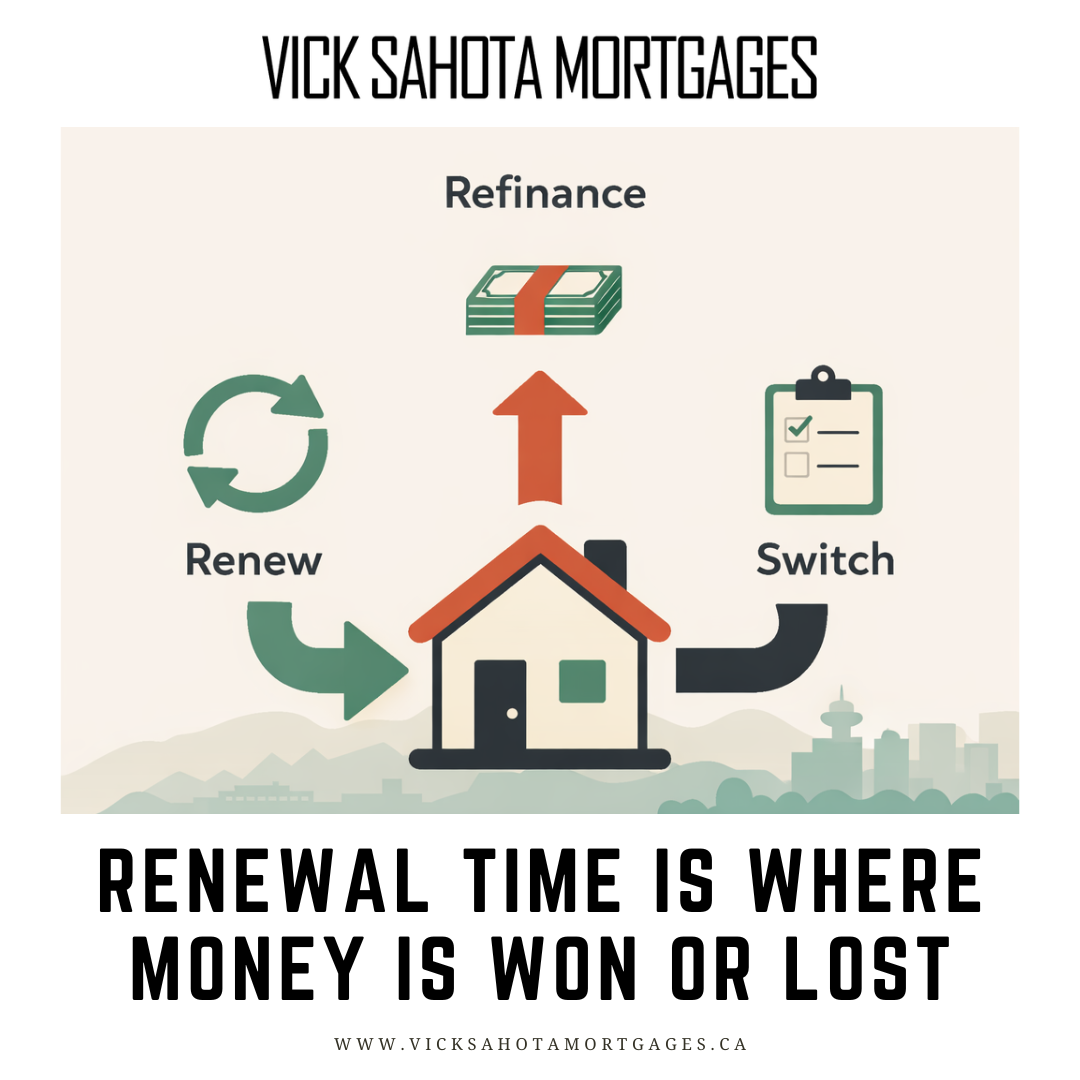

Your Three Options: Renew, Switch, or Refinance

When your maturity date approaches, you essentially have three paths, each with their own pros and cons.

Option 1: Renew

What It Means: Staying with your current lender under a new term and rate.

Best For: Homeowners who have experienced a job loss or credit drop and might struggle to requalify with a new lender.

Option 2: Switch (Transfer)

What It Means: Moving your exact remaining balance and amortization to a new lender.

Best For: Those looking for a better rate or product with another lender.

Option 3: Refinance

What It Means: Breaking your current mortgage to create a new one. You can access equity or stretch your timeline.

Best For: Homeowners needing to consolidate debt, access cash for investments, or significantly lower their monthly payments.

The "Maximum Flexibility" Refinance Strategy

When your mortgage is up for renewal, it is the best time to qualify for more credit, because the best time to qualify for more is when you don't urgently need it.

A highly effective strategy is to refinance and re-amortize your mortgage to the longest allowable timeline (e.g., 30 years). Why? Because it gives you the lowest possible contractual payment. Once you have that low baseline, you can use your prepayment privileges to manually increase your payments to match a shorter amortization (like 20 years). This puts you in total control. If you ever run into cash flow issues, lose your job, or decide to turn your property into a rental, you can instantly drop your payments back down to the required minimum. It is the ultimate financial safety net. You can also use a refinance to tap into equity to consolidate high-interest debt or invest.

Payment Shock Planning

If you are coming off a fixed rate from 2021, your new rate in 2026 will likely be noticeably higher. This difference can create a significant payment increase.

If your current budget cannot handle a massive jump in your monthly payment, the re-amortization strategy mentioned above is your strongest shield. By extending your amortization back out to 30 years, you can absorb the impact of the higher interest rate and keep your monthly cash flow stable.

Note: Extending your amortization does mean you will pay more total interest over the life of the loan. It is a trade-off between long-term interest costs and immediate, day-to-day cash flow survival.

The Renewal Negotiation Checklist

Do not let your bank rep dictate the terms of your financial future without answering some tough questions. Before you agree to stay with your current lender, ask them:

Will you monitor my mortgage after closing for savings opportunities?

If rates drop, will you proactively reach out to me to lower mine?

Will you check in with me annually to see if my mortgage still aligns with my life?

If I take a fixed rate today, will you help me plan to minimize the penalty if I need to break it later?

What specific strategies do you have to help me pay less interest over the life of this loan?

Have you ever contacted a client to let them know they could save money?

Will you personally be there to guide me during my next renewal in a few years?

If the answer to most of these is "no" or "I'm not sure," you are putting your biggest debt into the hands of someone who works for the bank. In this case, it will be up to you to manage your mortgage and ensure that you're making the right decisions, as the wrong ones can be costly.

Time to Update Your Strategy

Renewal time isn't just about interest rates; it's a forced checkpoint to review your overarching wealth strategy. Ask yourself:

What are my goals for the next 3 to 5 years?

How is my household cash flow right now?

Will I be selling this property soon, or converting it into a rental?

Do I want to make my mortgage interest tax-deductible?

Would an all-in-one offset mortgage work for my situation?

Let's Build Your Playbook

If you are facing a mortgage renewal in Vancouver, do not navigate it alone. I would be happy to assist you, run the numbers on your specific scenario, and put you into the best possible situation. My goal is to ensure you make the right decision for your family and receive proactive guidance leading up to, and long after your closing date. Click the link below to book a call.