Who Is Actively Managing Your Mortgage in Vancouver, South Surrey & White Rock?

Most homeowners only think about their mortgage at two points: when they first get it, and when it comes up for renewal. The years in between are usually treated as a stretch where nothing needs attention. Unfortunately, that gap is where a lot of money is quietly lost, and it is the part of the mortgage process that gets the least support.

For homeowners in Vancouver, South Surrey, and White Rock, where property values and mortgage balances are among the highest in the country, the cost of being left on your own through the middle of a term is real. The difference between a mortgage that is actively managed and one that is left to sit can easily add up to thousands of dollars over time.

The Reality of Bank Mortgages After Closing

If you get your mortgage directly from a traditional bank, the after-closing support is usually non-existent. The deal is funded, the file is closed on their end, and you are essentially left on your own to manage your mortgage and make the right financial decisions.

No one reaches out to check on your situation, flag a potential penalty issue before it becomes expensive, or tell you what the housing market is doing relative to the rate you are currently sitting on.

The result? Many homeowners only revisit their mortgage when the renewal letter arrives in the mail. By then, the chance to make a better, money-saving decision earlier in the term has already passed.

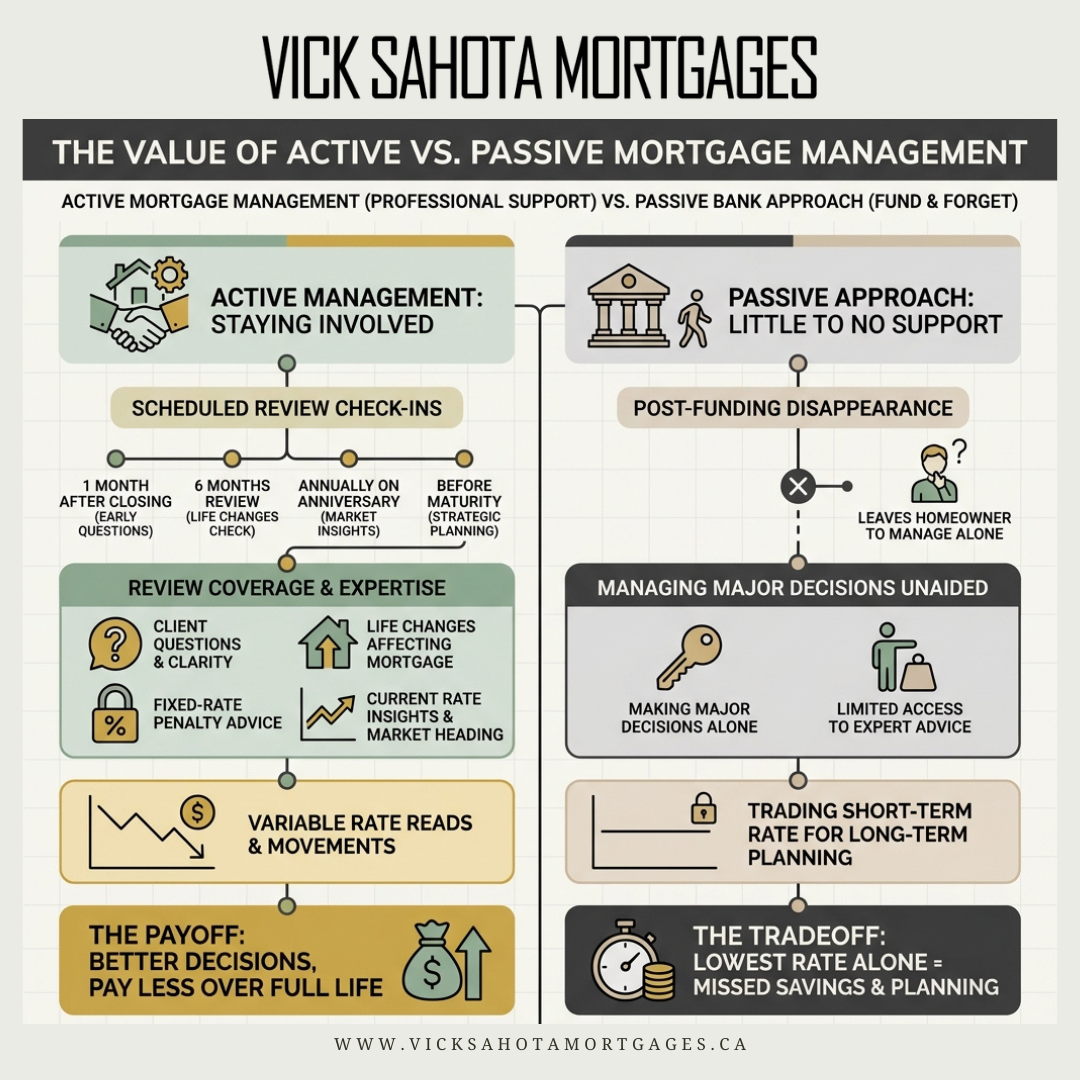

What Proactive Mortgage Management Looks Like

When you work with me, I don't disappear after closing. In fact, this is the part of our relationship that matters most. On a typical file, I implement a series of strategic mortgage review check-ins:

One month after closing.

Six months after closing.

Annually on your anniversary date.

A series of reviews prior to your mortgage maturity.

During these reviews, I check in to see if you have any questions or if there have been any major life changes that might impact your mortgage. We will look at penalty calculations for fixed options, and I provide insights into both your current rate and the broader market. If you have a variable rate mortgage, we’ll touch on where the Bank of Canada rates could be heading and what that means for your household budget in the months ahead.

Each of these conversations is an opportunity to make a decision while there is still time to act on it. A penalty that looks expensive today may actually make financial sense once the math is laid out. A life change, such as a growing family, a move, or a shift in income, often changes what the ideal mortgage structure should be. None of that gets caught when no one is actively looking at your file.

Beyond the Lowest Rate: The Value of Long-Term Strategy

It is easy to shop for a mortgage on rate alone. A bank or lender quotes a number, the number looks good, and the decision feels simple. The problem is that the lowest headline rate at the start of a term tells you very little about what the mortgage will actually cost over its full life.

When you choose a mortgage purely on the introductory rate and accept no ongoing support, you're trading a short-term win for long-term advice and planning. Your rate might be fixed for a few years, but the decisions that come up during those years, around penalties, prepayments, refinancing, and renewal timing, are where the larger dollars are truly won or lost.

Why Active Management Matters in Vancouver, South Surrey, and White Rock

Mortgage balances in the Lower Mainland and Fraser Valley markets are large enough that even minor decisions carry real financial weight. A miscalculated penalty, a renewal that is signed too early, or a missed prepayment opportunity can mean a difference of thousands of dollars across a single term. Active management is what keeps those decisions in view instead of leaving your equity to chance.

With my clients, I have the exact details of their specific situation. I use that data to help them make the right decisions and pay less interest over time. But that level of savings only happens when a professional is actively reviewing and managing the mortgage throughout the entire term, not just on day one.

Book a Call

If you want to pay less for your mortgage over time, you need to know that you have a professional in your corner helping you navigate the market and make the right decisions. Ready to get more out of your mortgage?