Vancouver Homeowner with a Rental Suite? Turn Your Mortgage Into a Tax-Deductible Wealth Tool

If you’re receiving rental income and have a mortgage on your primary residence, you’re probably not maximizing cash flow for the best tax efficiency. Often, when people receive rental income, they use it to pay down the mortgage on their rental. While this makes sense, it’s not the most optimal way to go about it.

With rental cash damming, you use the rental income to prepay the mortgage on your primary residence. With the right mortgage structure, the HELOC in the readvanceable mortgage opens up by the same amount, and you borrow from this line of credit to pay the mortgage and expenses on the rental property. The result? Over time, you’re converting the mortgage on your primary residence into a tax-deductible loan, one that can help generate yearly tax refunds. These tax refunds can then be used to pay down the mortgage on your primary residence. With this approach, you can convert your mortgage into a tax-deductible loan, generate yearly tax refunds, and knock years off your mortgage amortization.

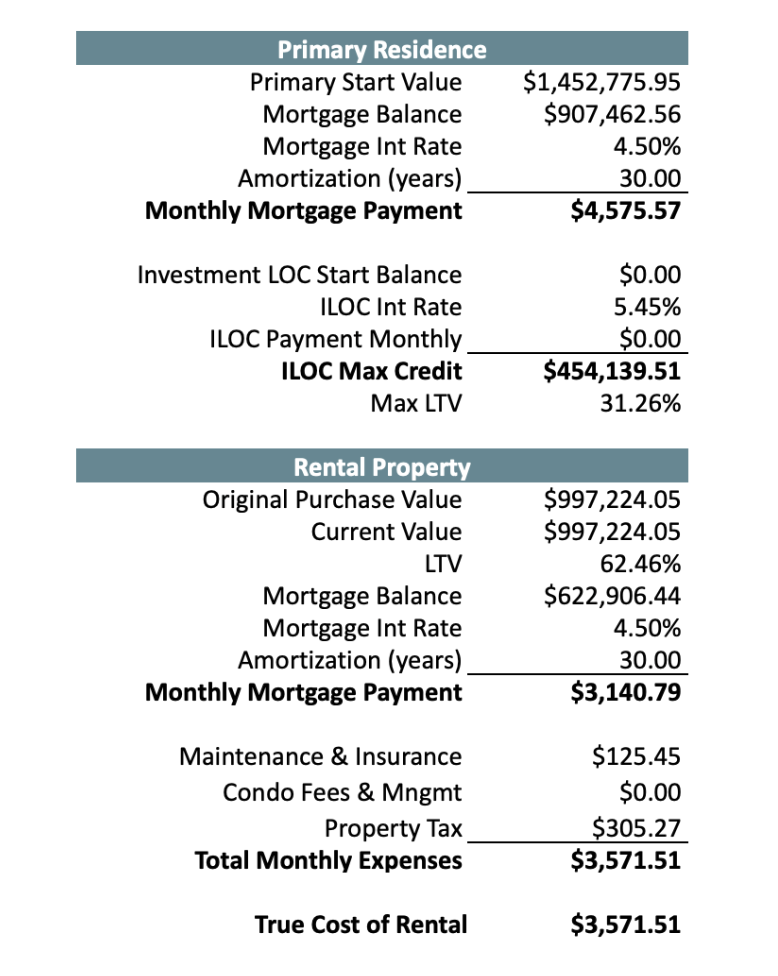

Did you also know this can be accomplished with a primary residence that has a rental suite on the property? The process is similar, but your mortgage needs to be structured properly and allocated separately between the primary residence portion and the rented portion. Consider this scenario:

A single-family dwelling with rental suites. The property is worth $2.45 million, and the mortgage on the property is $1.53 million, on track to be paid off in 30 years. About 40% of the property is rented out, so 40% of the mortgage and property expenses are already tax-deductible. This property receives $5,650 in monthly rental income. Let’s assume a rental cash flow appreciation rate of 2%, and the borrowers are in a 34.65% marginal tax bracket.

By splitting this mortgage into multiple components and implementing rental cash damming, the non-deductible mortgage can be fully converted into a tax-deductible loan in 8.75 years. The total tax refunds generated would be $58,596.95. This strategy would reduce the total number of mortgage payments by 190, which amounts to $869,358.30 in mortgage payments that no longer need to be made. And remember, mortgages are paid with after-tax dollars. To make $869,358.30 at a 34.65% marginal tax rate, you’d need to earn over $1.3 million in pre-tax income, which is all avoided with this strategy.

Lastly, once the mortgage is fully converted to a tax-deductible loan, if the same monthly mortgage payments are then used to pay down this loan, you’ll pay it off in just over 14 years. With no new cash out of pocket, you can accomplish all of this and knock over 7 years off your mortgage amortization.

There are a lot of nuances with this strategy, and it requires that the mortgage be set up correctly, but the results can be substantial. In Vancouver and the surrounding areas, it’s common to rent out a basement suite, and this strategy can be implemented if you have a rental suite. You’ll also need to work with a team of professionals, including an accountant. If you’re looking to implement this and other strategies to pay down your mortgage faster, reach out.

This isn’t tax advice. This blog post is meant to showcase the benefits of rental cash damming in this situation.